By Joe Allbright, Yair Babad, Doyin Famodu, Carl Ghiselli, Roseanne Harris, Walter Marsh, Susan Mateja, Bode Olajumoke, Muyiwa Tegbe

Editor’s note: This is the sixth in a series of articles from the Health Practice International Committee on ideas from foreign models of health care that may assist the United States in finding cost-effective ways to deliver high-quality health care in an equitable and sustainable way.

The region consisting of Africa and the Middle East, contains some of the richest economies in the world along the Persian Gulf, as well as some of the poorest in sub-Saharan Africa. Some of the oldest cultures in the world have—as a result of colonization, independence, and civil war—some of the youngest governments. The level of available national resources for health infrastructure and social programs vary widely, as do the population health outcomes.

Inequality is a thread that seems to connect many of the countries of Africa and the Middle East—whether it is on the basis of income, nationality, race, or religion. These factors compound the challenge all nations face to both design and gain political support for a health system that meets the needs of all populations within a country.

The region has been devastated by communicable diseases (e.g., HIV/AIDS, malaria, tuberculosis), conditions having to do with sanitation or poor access to health (e.g., diarrheal disease, malnutrition, infant and maternal mortality), and violence/injury. As population health improves, the burden of noncommunicable “lifestyle” diseases —such as cancer, respiratory disease, diabetes, and heart disease—will rise.[1]

Health systems will be challenged to adapt to the changing needs of the populations they serve. Below we examine four nations within this region, and their different approaches to health care.

Qatar

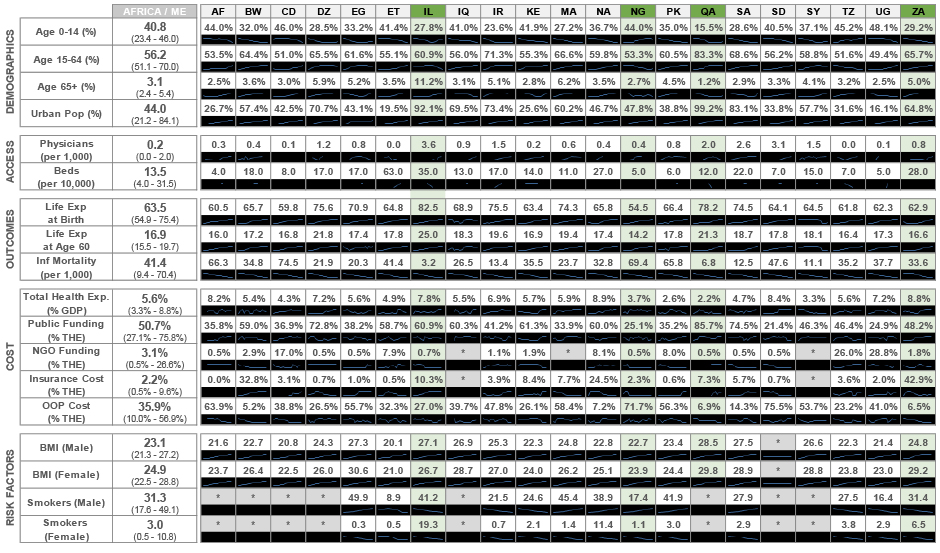

While there are many countries all over the world with developing health care systems, few have the economic resources of Qatar. Consistently ranked No. 1 or 2 in GDP per capita,[2] this small nation’s newfound petroleum and natural gas revenues have affected every aspect of life, including the provision of medical care. Qatar is estimated to have around 2.5 million people; 300,000 are nationals/citizens, 800,000 are white-collar expatriates and their families, and the remainder are (predominately male) blue-collar expatriate workers.[3,4] Qatar’s population has more than doubled in the last decade,[3] primarily as a result of the growing number of foreign workers needed to support the massive infrastructure projects.

Hamad Medical Corporation (HMC) is the national network of government-owned hospitals and health care providers; it is the main provider of health care and is accredited by globally recognized organizations. HMC was established in 1979 by Emiri decree and continues to grow, with new hospitals opening in 2017 and ambitious expansion plans through 2030.[5] While HMC is by far the dominant provider, a number of private hospitals also provide additional access for patients. As a general rule, the sickest, most complex patients go to HMC, as private hospitals are often not licensed to perform all services.

Qatar’s health care system is run by the Ministry of Public Health (MoPH), and reports similar population health outcomes to those experienced in North America. Life expectancy in Qatar is slightly longer than in the United States, and infant mortality rates are lower. These results were achieved while spending a much lower portion of gross domestic product (GDP); however, as Qatar has the largest per-capita GDP, this statistic is a bit skewed. In addition, there is ongoing research into disparities in care between the Qatari nationals and the broader expat community.[6] This can also be evidenced as the MoPH has contracted with the Qatar Red Crescent society to build three new hospitals specifically for the single laborer community.[7] While these hospitals will provide additional medical access as well as free up space at HMC, they also serve to segregate this population except in the most severe and complex cases.

The Qatari government funds over 85 percent of the care performed in Qatar. Currently, universal health care is available to all (HMC providers only), and everyone needs a health card in order to access services;[8] this card costs under $30 USD for expats and under $15 USD for nationals. There is private insurance available, though the advantages to purchasing are limited, and include gaining access to the private hospitals, which have more space and are more comfortable. Many nationals as well as white-collar expats have purchased private insurance, though much of the complex care is still provided at HMC through the health card, not the private programs.

Efforts to begin shifting the cost of care to individuals and employers have begun, though have stalled. In 2013 the MoPH initiated a private health insurance scheme for all residing in Qatar, rolling out first to women and children and then all Qatari nationals.[9] However, in a sudden reverse in direction, the scheme was canceled prior to full implementation in December 2015. The announcement was made in December, with scheme closure effective nearly immediately. This closure was partially attributed to a potential budget deficit, though provider abuse of the nascent scheme has also been mentioned in conjunction with the closing. These issues highlight the difficulties in implementing change, even with significant economic resources.

Qatar is a country of vast resources and has imported technology and health care ideas from around the world. Recent investments include the creation of a medical school and implementation of a national medical health record system. While Qatar’s is a developing health care economy, it faces unique challenges in both access for all residents as well as how to use those resources in the most targeted manner to achieve the highest-value outcomes.

Israel

Israel has a population of 8.8 million, a 10-fold increase from its founding 70 years ago. It has many ethnically and religiously distinct population groups, including 75 percent Jews and 21 percent Arabs (including Muslims, Christians, Druze, and Bedouins).[10] Among the Jewish population, 66 percent are secular, 25 percent are religious, and 9 percent are ultra-religious. These demographics are important for the Israeli health care system—with its emphasis on an equal and broad health and safety net for all its populace—as these groups differ materially in their cultures, socioeconomic status, fertility, and health status.

The life expectancy in Israel is 82.5 years. This is not only exceptional for the region, but it’s one of the highest in the world. As a result, the country is expected to age in the coming decades; a demographic change that the health care system will need to address. Unlike many of the aging populations in Europe and Asia, however, Israel has a high fertility rate. With 3.1 children born per female, driven by the ultra-orthodox and Bedouin communities, Israel is expected to be able to soften the burden of a growing number of elderly.

An important consideration for the Israeli health care system is the distribution of the population. The population is highly urbanized, with 41 percent living in less than 7 percent of the country’s area. Most of this is in the central district, Tel Aviv, and Jerusalem. To the south is the Negev desert, an area of very low population density, and home to the majority of Bedouins. The North, an area with a larger Arab population, is neither as urban as the major cities nor as remote as the south.

There are four health maintenance organizations (HMOs) in Israel (called “Sick Funds”) that provide free primary and secondary care to Israelis. One HMO covers the whole country, while the other three have non-uniform services both in wait times and geographical distributions. As each resident may be a member of only one of these HMOs, this unequal availability makes mobility between regions—due to work, family, education, and other reasons—harder, and makes the non-urban areas and non-major localities less desirable.

These ethnic, demographic, and population issues complicate the management of the Israeli health care system, whose basic precept is specified in Article 1 of the 1995 National Health Insurance Law (NHIL): “The National Health Insurance is based on the principles of justice, equality, and mutual assistance.” This ideal is in line with Israel’s creation as a social-democratic state, with strong community support and recognition of the state responsibility to all its citizens. The law provides universal mandatory coverage to all Israeli residents, who are free to move between the HMOs. Each HMO offers comprehensive medical services and a national medications basket that is updated annually.

Inequality in Israel, and its health care implications, is indeed one of the major risk factors faced by the health care system. While both Arab and Jewish populations in Israel are in great health relative to the rest of the world, life expectancy among Israeli Arabs is 79.0 years versus Israeli Jews at 82.7. Infant mortality among Israeli Arabs is 6.1 per 1,000 births, versus 2.2 for Israeli Jews.[10] A major source of inequality is said to be the lack of understanding of the system and what it provides by most of the population, and in particular the lower socioeconomic groups. Poverty, with threshold defined as 50 percent of median equalized disposable income in the country, is highest in Israel relative to the countries in the Organisation for Economic Co-operation and Development (OECD)[11] both for the elderly and for the whole population.

The health care system is taking steps to reduce the inequality, both at the Ministry of Health level and at the HMOs level. These steps also address other cost drivers; long-term care, chronic morbidity, and the costs of medical advances and technology. Multiyear educational, operational, infrastructure, and regulatory plans and projects, as well as reforms, address the inequalities noted above for age groups (and particularly the aged), for communities (with emphasis on peripheral communities and ethnic groups), and for service levels. A particular emphasis is placed on education of new medical professionals (whose number is declining with the aging of the population and the reduction in emigrating medical professionals), and on funding and building new infrastructure facilities to match the population growth.

Consistent with its founding principles, the NHIL—particularly its safety net—relies strongly on community volunteerism and support. As Israel has moved toward a more capitalistic economy, however, funding challenges have arisen to keep the system equal, accessible, and affordable. The NHIL has three sources of funding: a salary-based health tax of 9.5 percent up to certain income (53 percent of funds), the government budget (41 percent of funds), and, finally, by user charges (6 percent of funds).[12] The reliance on the national budget results, as well as the ever-increasing needs and costs of the health care system leads to the system being in continual deficit.

While the NHIL provides comprehensive coverage from pre-conception to death, it provides limited preventive, geriatric, psychiatric, dental, and long-term services. Further, some of the services assured by the law (such as certain elective surgeries) have long wait times and do not provide desired options such as selection of a surgeon. The HMOs therefore, with the permission of the law, developed supplementary services, to respond to these needs. Each of these services is managed as an age-subsidized collective coverage. They cover about 75 percent of the population—which implies that about 25 percent of the population do not receive these services—and increase the inequality of the system. Similarly, the HMOs each provide a collective age-subsidized long-term care coverage, in which about half of their members participate.

A third layer of health care is provided by private insurance, with dread disease, transplants, medications not covered in the NHIL’s medication basket, travel insurance, and other coverages. It covers about 43 percent of the population, which implies that many people have multiple coverages—by the NHIL, the supplementary services, and their private policies. As the private insurance is usually too costly for the lower socioeconomic echelons, this further reduces the equality of the Israeli health care system.

Israeli regulators introduced several major reforms over the past several years. They introduced a standardized private medical insurance policy, canceled private collective long-term care (LTC) insurance policies, and are now in the process of consolidating all the LTC coverages in Israel—within the framework of the HM LTC policies and possibly through consolidation with the NHIL.

The Israeli health care system demonstrates both the benefits and challenges of a universal broad coverage to all residents. It is characterized by a pursuit of equality of access, availability, and outcomes among all the constituents of the population, as well as quality of outcomes, while at the same time struggling with the funding of the system within a free market that provides both for national health system and a strong and powerful insurance market.

South Africa

The South African health care system is broadly divided into a public and private sector. Sixteen percent of the population (8.9 million people)[13] are covered by medical schemes—regulated, nonprofit entities providing indemnity-based medical coverage—which may be restricted to a particular employer or industry or may be open to all who apply. A further 10 million South Africans are not covered under a medical scheme and use private health care providers on an out-of-pocket basis. The balance of the population (approximately 38 million people) depend on public-sector health services. Public-sector health services are means-tested (although this is not rigorously applied) and tend to be associated with long waiting times and service delivery challenges.

The private-sector medical schemes operate on a social solidarity basis with open enrollment, community rating, and prescribed minimum benefits (covering acute incidents, urgent care, and chronic disease management). The low levels of coverage by medical schemes is primarily due to affordability constraints. World Bank reported that South Africa is “one of the most unequal countries in the world,” citing the challenges of high poverty, high income inequality, and high unemployment.[14] Nonetheless, a greater share of total health expenditure is spent on private insurance in South Africa (43 percent of total health expenditure) than any other country in the world.

The burden of disease in South Africa is dominated by the HIV epidemic and associated tuberculosis (TB) prevalence. Reference is frequently made to the “quadruple burden of disease” in South Africa which refers to (1) HIV/AIDS, TB, and other communicable conditions; (2) maternal and perinatal conditions; (3) violence and injuries; and (4) noncommunicable diseases.

The rollout of a comprehensive antiretroviral treatment program (following years of HIV denialism) has led to a significant decline in mortality associated with HIV/AIDS and tuberculosis since 2006. The creation of a mother-to-child transmission prevention program has reduced infections and infant deaths. These improvements are reflected in South Africa’s improved life expectancy (from 57.1 in 2009 to 63.8 in 2016) and reduced infant and maternal mortality rates (from 39 per 1,000 live births in 2009 to 25 deaths per live births in 2016). HIV/AIDS still accounts for almost half of all premature mortality (population prevalence was estimated at 12.6 percent in 2017)[15] and so the ongoing commitment to sustaining and strengthening these programs is essential.[16]

The burden of noncommunicable diseases, particularly cardiovascular diseases, diabetes, chronic obstructive pulmonary disease (COPD), and cancers is expected to escalate with an ageing population. The National Department of Health has adopted a strategic plan for prevention of these diseases, which has included taxation and usage restrictions associated with tobacco-related and sugar-laden products. There is extensive public debate on some of the proposed measures.

The public health care system includes hospitals and clinics that are funded through allocations to provincial health departments in the nine provinces. This leads to disparities in service delivery across the country and concerns about the quality of care and adequacy of resources. In KwaZulu Natal, for example, public-sector-provided oncology has come to a standstill, and there has been a much-publicized lapse in governance for mental health care services in Gauteng.

The policy trajectory is to develop a national health insurance framework with a single public fund approach. This undertaking would centralize all health funding into a single pool, which would then purchase care from health care providers in the public and private sector. The medical schemes could continue to play a complementary role to this national fund. There is much debate about the affordability and feasibility of such a model, but there is a consensus that some approach to reform of the health care system to improve delivery of care to all South Africans is critical.

The Competition Commission has been conducting an inquiry into the operation of the health care market since 2014; provisional findings were released in July 2018.[17] This inquiry has focused on the private sector, which includes hospital groups, funders, and private practitioners. The dominance of three large hospital groups is under some scrutiny, as are the professional body rules that prevent doctors and specialists from being employed by hospitals or structuring multi-disciplinary practices. The report found that there is a need to move away from fee-for-service remuneration and facilitate more innovative contracting mechanisms. The high levels of inflation in the cost of private health care services is also said to be attributable to anti-selection as the social solidarity framework under which medical schemes operate is not complemented by any mandatory cover requirements or risk equalization mechanism.

While South Africa is spending over 8.8 percent of GDP on health care, only half of this spending is in the public sector (funded by tax revenue), while the balance is primarily made up of voluntary contributions to medical schemes and some out-of-pocket expenditure. The high proportion of private health insurance thus reflects the propensity of higher-income earners to purchase medical scheme coverage rather than to use public facilities, as well as the higher cost of private medical care compared to the public sector.

There seems to be significant opportunities for efficiency gains in the delivery of health care in the private sector in order to make cover more affordable as well as the opportunity for more public-private partnerships in delivery of care to expand access to quality care. The regulatory environment for health care in South Africa is thus currently undergoing a process of extensive scrutiny and reform.

Over the past decade, South Africa has seen major improvements across many population health measures. Many of these gains are the result of a targeted approach to address particular national health issues. In order to build on this success, however, South Africa will need to find a path to offer consistent and high-quality health care in an environment of high economic inequality.

Nigeria

Nigeria’s health care delivery system is composed of a public system, largely funded by government revenues, and a system of small- to medium-sized privately owned facilities, typically operated as sole proprietorships. The public health care system is three-tiered, with funding and operational responsibilities separated according to the levels of government. The federal government funds the delivery of tertiary care through a network of university-affiliated teaching hospitals and federal medical centers located in the 36 administrative capitals of each state and in Abuja, the federal capital territory. The state governments are responsible for funding the delivery of secondary care at general hospitals located in each local government area of their respective states. Local government councils are required to fund the delivery of primary care services at primary health care centers, dispensaries, and health posts. This health care delivery structure evolved over time through a series of laws and national development plans.[18]

Prior to 2005, payment for health care services was predominantly out-of-pocket. Individuals and families had to make full or partial payment to providers before services were rendered, irrespective of the nature of the medical urgency or emergency. The federal government attempted to address financing of health care in Nigeria with the introduction of the National Health Insurance Scheme (NHIS) in 2005. The main objective was to create a sustainable health care financing system and provide universal health coverage to all citizens.

The NHIS started out by accrediting eight health maintenance organizations (HMOs) in 2005, and has grown to approximately 85 HMOs and health insurance companies currently in operation. The HMOs are modeled after the payer organizations in the United States operating as HMOs, preferred provider organizations (PPOs), exclusive provider organizations (EPOs), in open panel, closed panels, or staffing provider network, providing different levels of prepaid products to government employers, large private employers, and individual clients. The predominant products marketed are facility-capitated arrangements with elaborate pre-authorization, utilization reviews, and case management as the core of their cost containment strategies. A few payers offer fee-for-service products that require stop-loss, surplus treaty, and reinsurance products, to manage risk. It has also created the demand for human capital development that will be the core of organizational, operational, financing, IT infrastructure development, and growth for health care delivery.

Funding for health care in Nigeria has been historically poor, with total health care spending in 2014 at just 3.7 percent of GDP, which is one of the lowest in sub-Saharan Africa. This chronic underfunding has resulted in the poor state of government-owned health facilities, poor quality of care delivery, and poor health outcomes. Consequently, Nigeria has one of the world’s lowest life expectancies (at 54.5 years) and one of the highest infant mortality rates (69.4 per 1,000 births).[19]

The private sector has also been unable to bridge the care delivery gaps. A primary reason behind this inability has been that because most private facilities, as sole proprietorships, often lack access to the private financing required to fund the establishment of modern facilities or purchase modern diagnostic or therapeutic equipment, limiting the range of services they can offer and the extent medical personnel can go to treat their patients and preserve lives. As a consequence, there has been significant erosion of trust in Nigeria’s health systems by a vast majority of the populace.[20] Middle- to high-income earners now seek health care services outside Nigeria, resulting in significant capital flight—medical tourism—out of the country. Conservative estimates put the cost to the Nigerian health care system in excess $1 billion annually.[21] Furthermore, health care personnel, especially doctors, leave Nigeria in large numbers due to lower remuneration and poor working conditions.

The establishment of the NHIS provided an opportunity to improve the financing mechanisms in Nigeria and improve health outcomes. However, the implementation and adoption of the scheme has been slow. Enrollment is currently at just 5 to 7 percent of the population across all participating HMOs. The poor penetration of the NHIS only ensures that out-of-pocket health care costs remain as high as 72 percent, while private insurance pays only 2.7 percent of health care expenses.

The enabling legislation of the NHIS did not create a structure and incentives that would have ensured broader participation. Two critical factors that prevented wider adoption were 1) enacting the NHIS as a voluntary participation scheme for individuals and employers; and 2) the lack of implementation roles for states and local governments.

To bridge this gap in the national system and provide insurance coverage for their citizens, states chose to go it alone by creating innovative state-based universal health care programs. States like Bayelsa, Lagos, and Ondo are at the forefront of compulsory contributory schemes that provide subsidy-based financing to drive enrollment.

With a population of over 180 million, significant work is required to create a health care delivery system that meets the needs of the population and is attractive to investment. Above all, the need for reliable data is necessary to determine how funds should be directed. Nigeria’s health care data is currently largely uncollected and unreliable. Data collection could be enhanced through the deployment of electronic medical record systems at point of care, development of disease registries, immunization registries, and collection of utilization and pricing data. The unavailability of these data has for years hampered adequate planning, outcomes evaluation, and limited capital inflow because investors could not make decisions in the absence of good industry data.

Lessons for the United States

The nations examined here all exhibit similar challenges to those faced by the United States, in exaggerated fashion. Qatar’s goal of universal coverage was at odds with the financial and political costs as it extended the program to more of its population. Qatar is consciously making large investments in its national health care infrastructure—though the investment is during favorable economic times. The Affordable Care Act likely faced greater financial pressure, coming as it did on the heels of a U.S. recession.

South Africa and Israel both face the challenge of aligning a public health system with a private one. Private systems tend to capture the lowest risk and the majority of the funds, leaving the public system both overburdened and underfunded. Additionally, the availability of private or supplemental coverage to those who can afford it makes it harder for those in a position to make such decisions from appreciating the access issues for the population who cannot afford better access.

While Israel and Qatar are experiencing the benefits of medical tourism, Nigeria reminds us of the other side of that equation. While there are regions in the United States with world-class medical centers, that means that a significant amount of medical capital and talent are being drawn from poorer and more rural areas. Nigeria’s system of funding primary care locally, secondary care regionally, and tertiary care nationally recognizes this fact.

Finally, we saw examples of how “success” in managing population health often needs to be followed by a pivot. After South Africa’s improvements in infant mortality and communicable diseases, the system needed to be prepared for the increasing need to address lifestyle diseases. As Israel improves the average life expectancy of the population, there becomes a greater need for LTC services. Health systems need to be flexible enough to change with the population.

References

[1] Global Status Report on Noncommunicable Diseases 2010; World Health Organization; 2011. [2] “RANKED: The 30 Richest Countries in the World”; Business Insider; March 6, 2017. [3] The World Bank: Data. Retrieved from data.worldbank.org/country/Qatar. [4] “Population of Qatar by Nationality—2017 Report”; Priya Dsouza Communications; Feb. 7, 2017. [5] “HMC’s Current Expansion Phase the Largest in the History of HMC Hospitals”; Hamad Medical Corporation; Nov. 24, 2016. [6] International Journal of Clinical Medicine; 177-185; March 2015. [7] “Three New Hospitals for Single Workers”; Gulf Times; Aug. 4, 2013. [8] “Patient Information—How to Get a Health Card?”; Hamad Medical Corporation website; undated. [9] “Sudden Closure of Qatari National Health Insurance Scheme”; International Medical Travel Journal; March 3, 2016. [10] The Health of the Arab Israeli Population; Taub Center for Social Policy Studies in Israel; December 2017. [11] OECD Income Distribution Database. Retrieved from oecd.org/social/income-distribution-database.htm. [12] “Exploring Global Health Cost Drivers: Israel and the Netherlands” webinar; American Academy of Actuaries and International Actuarial Association Health Section, Feb. 18 2015. [13] Health Matters; Council for Medical Schemes Annual Report 2016/2017. [14] Overcoming Poverty and Inequality in South Africa: An Assessment of Drivers, Constraints and Opportunities; World Bank Group; March 2018. [15] “Mid-year Population Estimates 2017”; Statistics South Africa; July 31, 2017. [16] “Mortality Trends and Differentials in South Africa From 1997 to 2012: Second National Burden of Disease Study”; The Lancet Global Health; September 2016. [17] Health Market Inquiry—Provisional Findings and Recommendations Report; Competition Commission South Africa; July 5, 2018. [18] “The Evolution of Health Care Systems in Nigeria: Which Way Forward in the Twenty-First Century?”; Nigerian Medical Journal; Nov. 27, 2010. [19] World Health Organization Global Health Observatory data repository. [20] Restoring Trust to Nigeria’s Healthcare System; PwC; 2016. [21] Nigeria: Health Budget Analysis; BudgIT; 2018.