By Allen Ellstein

The following article discusses the history of mutual funds and what we can learn from it. While funds have been around since the 1920s, it was only in the 1950s that they started to become a popular vehicle for the average investor. Unless otherwise stated, the funds discussed are considered to invest in large capitalization companies.

In looking at the period 1950 to the current date, I will use several sources of information.

First, the seminal work that Forbes magazine did in the 1970s. Each year in the second issue of August, it did an annual mutual fund review. I re-examined the Forbes run from 1970 to 1979 for this article.

Second, John Bogle’s wonderful history in the January 2005 issue of the Financial Analysts Journal titled “The Mutual Fund Industry 60 Years Later: For Better or Worse.”

Third, James Farrell’s article in the Journal of Business, April 1974 titled “Analyzing Covariation of Returns to Determine Homogeneous Stock Grouping.” This work was based on his 1971 PhD. thesis at New York University.

And finally, I draw upon my own long history with funds, which began as a consumer and continued in my work in the insurance industry starting in the 1970s.

Making the Grade

Forbes began to study mutual fund performance in 1962. By 1973 it had 11 years of mutual fund data to compare performance to the Standard and Poor’s 500. It was Forbes’ hypothesis that a long period of time was needed to see how funds compared to the overall market. Forbes looked at the overall return over that 11 years, and then graded mutual funds for up markets and for down markets compared to the S&P 500. At that time there were basically two fund styles: blend and growth. An example of a blend fund was Dodge and Cox Stock Fund. And an example of a growth fund was the T. Rowe Price Growth Fund.

Funds were graded A to F for two types of markets—up markets and down markets. A grade of C meant that the fund performed similar to the S&P. That is, the S&P got a grade of C for up markets and a C for down markets over that 11-year period. If the managers were kind of average, one would expect that a blend fund would get grades of C for up markets and C for down markets. For a growth fund, one might expect a B for up markets and a D for down markets. In the case of a growth fund, before expenses one would expect a higher rate of return than the S&P, as the fund had more risk of volatility (Beta risk). And in fact, many growth funds got grades of B for up markets.

In fact, unlike the past 15 years where funds did not beat out the index, the average mutual fund rated in 1973 by Forbes returned 6.3% versus 6% for the S+P. The period studied (1962–1973) was rich in data because there were some up and some down markets. Part of the 0.3% that funds had over the S+P, even after expenses, can be explained by the greater risk taken on by the growth funds—and part of it can be explained by the increasing popularity of growth funds, causing imitators in the second part of the period, pushing up the price-to-earnings ratio of growth stocks perhaps to levels beyond normal rationale (price–to-earnings expansion). Nonetheless, some of the excess return before expenses can be attributed to the managers of the day having some skills in picking stocks in the up and down markets of the time.

What’s In a Name?

It should be noted that boutique managers or investment committees had a longer tenure than they do today, so the funds could be considered to be more or less managed the same over the longer period. Today, with management turnover, it becomes more difficult to assess long-term management of a fund—it may not be the “same” fund over an 11-year period.

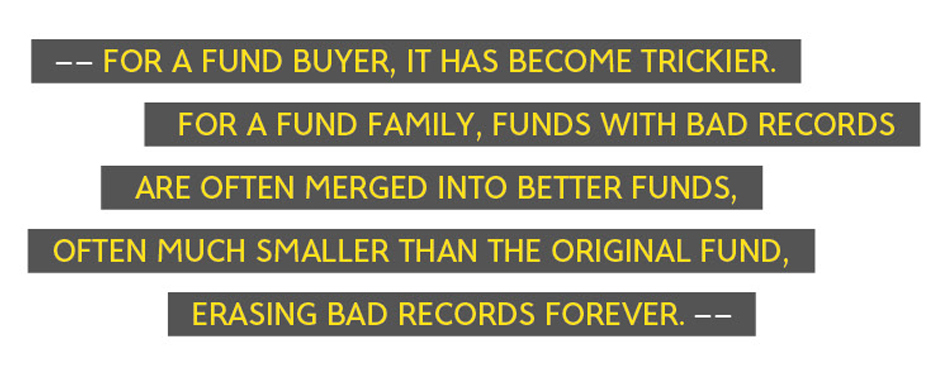

For a fund buyer, it has become trickier. For a fund family, funds with bad records are often merged into better funds, often much smaller than the original fund, erasing bad records forever. Even worse, as I saw in my work as a regulator, is that mutual funds or exchange-traded funds (ETFs) that did not work out could just be liquidated, meaning that a person who dollar-averaged into the fund effectively “sold” all shares at a single point in time.

Further, for some mutual funds or insurance products with surrender charges, a company would map the fund to another fund. Thus, a government bond fund could be mapped to a corporate fund, for example. In one case in a 401(k), I saw a real estate fund mapped into a stock fund. The Securities and Exchange Commission (SEC) criteria was basically that the new fund needed to have a better overall short-term record and a lower expense charge. Someone with a real estate fund or a Treasury fund bought it and dollar-averaged into it for a purpose, and they were now stuck with their strategy in tatters—and often a surrender charge if they wanted to get out of the replacement product.

It is interesting to note that when a fund is part of a sale, the original fund objective may stay the same, but as new managers are assigned, the first thing they do is to make a lot of changes in the portfolio and raise the expense charges in some way. One such change that I observed was a fund with an already too-large asset base sold to a financial firm. It immediately asked the shareholders to add a 0.25% 12B1 marketing fee so it could increase the assets under management. I wrote to the president that this was against the shareholders’ interest. He never wrote back, and there were enough votes and shares to override whatever small shareholders voted in any case.

Forbes did comment in 1973 that price-to-earnings expansion cannot continue forever. Today in what might be called the second wave of P/E expansion, one can point to a number of considerations. The original wave of investors that was drawn to stocks for the first time by being able to buy mutual funds probably has peaked, so it may not be much of a factor. But the move of companies to shutter their pension plans—which historically had only a relatively small amount in stocks (think bonds, mortgages, some real estate)—in favor of 401(k) plans with lots of stock options has created a demand for stock ownership, both in out of mutual funds, still seems to be in play.

Turnover Ratio

The turnover ratio for both mutual funds and the stock market was fairly benign and may have been in at a relatively low point in the early 1960s. The Forbes 1970 issue stated that before 1965 the average turnover rate for funds was about 16% compared to S&P 500 stocks of about 14%. Not surprising is that from the low point, the turnover rate of stocks went to 20% by 1969; it is perhaps surprising that mutual funds’ turnover ratio moved to an average of about 43% by that year.

Forbes and Bogle more or less concluded that when turnover rates approach 40%, there is more speculation than investing. Bogle stated that the average mutual fund had a 90% turnover rate from 1983 to 2003. However, for the funds that would be popular, in my opinion, the rate might be more like 50%, which is still very high.

In talking to experts over the years, I have struggled to come up with what good turnover ratios should be. In average markets, the consensus that I have heard for the typical fund for a typical year is 20% for a large-cap fund, 25% for a mid-cap fund, and maybe 30% for a small-cap fund.

However, one needs to be careful to understand the specific fund’s style in examining turnover rate. Many people initially avoided the Mutual Shares Fund because it had a turnover rate of 100% or so. But asset manager Max Heine was investing in distressed securities—his specialty—and thus a large turnover rate made sense.

The Changing Landscape

Turning to the work of John Bogle, we can add some richness to how funds, advisers, and individuals behave. Equity fund investors before 1975 were truly long-term investors, with an annual turnover ratio of about 6% to 10%. For a while after that, the rates went up significantly, but much of that was due to fund companies allowing favorite clients to try to make late-day trades after the so-called closing price had been set. The SEC fined the companies and the practice, if not eliminated, was greatly reduced. As of 2004, the turnover ratio sat at about 25%, meaning that the average fund investor only kept the fund for four years.

Several factors help explain the short time investors are sticking with a fund. First, people are using financial advisers much more now, and they tend to justify their fees (and get some commissions) by moving money from so-called underperforming funds to new ones. Secondly, with 401(k)s and the like, there are no tax consequences to moving money. Also, to the fund holder, the so-called fund supermarkets allow what appears to be free movement within funds in the supermarket. Of course, the funds pay to be in Schwab’s or Fidelity’s supermarket, and one way or the other, expenses go up.

Mutual funds, as Bogle points out, as of 2004 owned about 25% of all stocks, but they are not typically active in annual stockholder meetings—so corporate governance suffers. Between mutual funds voting with management and many companies giving more stock to senior leadership in the company, I think it is small wonder that C-suite pay is high and not tied to long-term performance.

As Bogle points out, up until 1958 mutual fund companies were kind of boutique companies, in it for the long run. Starting in 1958, the regulatory landscape changed and management companies could be on the stock exchange, or bought and sold by larger financial institutions such as banks and insurance companies. Original owners could now make money by selling their companies, and the new entities had to worry about stockholder return and return to the parent company. And each time a company was sold, the new entity had an incentive to both raise fees and push for more assets under management, rather than just run a set of funds. The game had changed from performance to creating more assets under management—and more fees.

In discussing expense ratios, Bogle points out that the average expense ratio for a fund grew from 0.76% in 1945 to about 1.56% in 2004.

The Cost of Doing Business

Bogle tested the theory that the average mutual fund underperformance relative to the market could be explained by the expenses it charged and the cost of trading. He studied two periods. For the period 1945 to 1965, the market returned 14.9% and the average stock fund 13.2%. The difference is 1.7 percentage points. He said that was almost the same as his estimated value of 1.6%, which consisted of 0.8% for expenses and 0.8% based on the costs of a turnover ratio of 16%. (The total costs of trading were higher than today but at a much lower turnover ratio.)

Bogle did a similar calculation for the period 1983–2003. The market returned 13% and the average mutual fund returned 10.3%, for a difference of 2.7 percentage points. He estimated that the average fund had an expense ratio of 1.4% and cost of trading of 0.9% for a total of 2.1%. Bogle does not discuss the 0.6-percentage-point difference, but active managers need to have a cash position, to cover people entering and exiting, and to have some flexibility to avoid overpriced stocks and markets.

Bogle’s 0.9% for the cost of trading for the period 1983–2003 was based on a 1% cost of trading on a portfolio turnover rate of 90% in 1993. This translates to about a 1.1% cost for selling one stock and buying another for the portfolio. This is similar to the 1.2% cost of a round trip trade that I estimated from looking at supplemental materials provided by mutual funds and talking to fund managers in the early 1990s.

The cost of trading, which includes all of the implicit and explicit costs, is of course much higher than the brokerage fee. Today, of course, the direct brokerage fee is less, and despite high-speed traders, the bid-ask spreads have not increased. The actual cost of trading can vary widely and the use of average numbers can be misleading. On a particular sell-and-buy trade, it might be as low as 0.2% and as high as 4%.

The history of broker costs in itself contains some unintuitive results. Often a mutual fund might not choose the lowest-cost broker or method to do the trade. This may be because the chosen broker can provide some services to the fund that are valuable given the large resources of the firm. Or, it could be because broker fees are not counted in the expense charge—this might be a way of getting a lower expense charge for use in the prospectus. Nevertheless, if one does not use some estimate, there is no way of comparing the expenses including trading costs for a low-turnover fund to a high-turnover fund.

For purposes today of comparing the costs of portfolio turnover, as a rough measure I tend to use 0.6% of the turnover ratio. For those who might want to be a little more precise, one might use 0.5% for a large-cap domestic fund, 0.7% for a mid-cap fund, and 0.85 for a small-cap fund. I would add 0.2% to those numbers for foreign funds.

For example, consider two large-cap funds with expense ratios of 0.6%. One might have an average turnover ratio of 20% and the other a ratio of 50%. The first would have a total cost ratio of 0.72% and the second a total cost ratio of 0.90%. At a 100% turnover ratio, the total becomes 1.2%.

An expense of, say, 1% might not sound like all that much if one is earning 10% gross. But let us compare a 0% expense to that 1%. For 0% expenses and a tax rate of 20%, that would leave an 8% net gain on that 10% gross. If inflation was at 3%, that leaves a net return of 5%. For the 1% in expenses, after expenses, one has 9%. With a 20% tax that leaves 7.2%, or 4.2% net of inflation.

It should be noted that some turnover for an active manager who is buying for the long term can be beneficial. If a stock is now too big a position due to excellent performance, then trading to diversify the portfolio is likely good. And secondly, if a stock has now reached what is considered a very high price for its underlying fundamentals, it might be time to reduce or eliminate it. Similarly, if a stock has disappointed, there may be better alternatives. Finally, if the market is uncertain, it might be time to go to more cash—one of the advantages of an active strategy over an index.

Other Ways of Grouping Stocks

Farrell attempted to figure out whether grouping large-cap stocks by similar performance could create a portfolio that did better than throwing darts at the market as a whole. Earlier attempts to stratify stocks by industry type had led to mixed results; it was not clear that stocks in the same industry acted more like one another than other stocks in the sample, or at least enough to get a better portfolio by making sure that each industry type was represented through the selection process.

Part of the difficulty with industry type can be seen with the food industry. In the 1960s a company like McDonald’s might act closer to other non-food growth stocks than it would with the more stable supermarket companies in the food industry.

What Farrell did was to use cluster analysis on 100 large-cap stocks—all that computers of the day could handle—and see which stocks behaved similarly. He ended up with four groups: growth, cyclical, stable, and a leftover group of mostly oil companies. Out of his 100 companies, 31 turned out to be growth stocks, 25 stocks were relatively stable when economic conditions changed, 36 were cyclical stocks, and eight were oil-like stocks.

Given this breakdown, he then went back to see whether grouping for industry within each group could further explain the movement of prices. For the period 1960–1969—and it will vary by period—he documented that 45% of the return of a stock was due to its unique characteristics, 14% was due to its cluster type (growth, cyclical, etc), 30% to market conditions, and 10% to the industry type, if one first stratified by cluster type.

The current period is very different from the 1960s. If we assume that the roughly 25% of stock return attributable to the clusters and industry factors does not change much, then what can vary is the 75% attributable to market forces and the unique company. History has shown that the factor for market conditions will increase when there is a material movement up or down in the stock market, often due to economic factors, and the factor for individual stocks will tend to decrease.

Currently, with both the popularity of index investing as a strategy and the rapid increase in stock indices, one can postulate that the market factor is up and the company factor is down. If in the past 10 years the market factor were 40% (due to both indexing and the rapid rise of stock prices, where we have seen P/E expansion) and the individual stock price factor was 35%, it would have been very hard for many truly active managers to have beaten an index fund, unlike the period of the 1960s.

What all this suggests is that a portfolio that has 30% in growth stocks, 30% in cyclical stocks, 30% in stable stocks, and 10% in oils, can under average conditions outperform (on a risk-adjusted basis) a totally random portfolio—and that if one stratifies for industry type within the clusters, one might do somewhat better.

As might be expected for the period 1960–1969, Farrell showed that growth stocks returned the most, but with the most volatility. Mainly, the monthly average returns for growth stocks was 1.56% with a standard deviation of 5.36% and a regression coefficient of 1.24. For cyclical stocks the return was 1.05% with a standard deviation of 4.51%. For stable stocks it was 0.86% with a standard deviation of 3.77%. And for oil stocks it was 0.86% with a standard deviation of return of 4.24%. Regression coefficients for other than growth were between 0.85 and 1.11.

The implication of these cluster groupings is that for a given level of desired risk (beta), a portfolio can be created and risk-adjusted that would be superior to just a random portfolio of, say, 30 stocks.

Key Takeaways

Given that today’s mutual fund industry seems to divide portfolio styles into growth and value, with the so-called blend strategy being an amalgam of both, what can we learn from the works of Farrell? First, growth is a style that is more or less well defined. But what is this thing we call “value”? Apparently, “value” is everything that is not growth. As such it includes stable, cyclical, and oil stocks. It might also include stocks from any of the four cluster groups—including growth, fallen angels, or stocks that have had bad events that a manager thinks they can recover from.

Given Farrell’s work, it would appear that managers in the value world would do well to identify and modify their portfolios to get a representative selection from the three non-growth clusters, possibly making sure to allow for some level of industry diversification within each cluster, if the number of stocks in the portfolio is large enough.

In summary, over the last 50 or 60 years we have seen the mutual fund industry change from a sort of independent, results-oriented industry to one defined where the “owners” are to a large extent rewarded by optimizing assets under management. Much of the action in the industry is the buying and selling of funds and fund companies, and corporate owners trying to make money for their direct constituents. The individual fund holder may come second.

Low portfolio turnover and low expenses can, for most strategies, increase returns to fund holders. Given the obfuscation on the true cost of trading, it is useful to calculate a total expense number to include an estimate for the cost of trading. Dividing up stocks into clusters that act similarly can potentially improve risk-adjusted results in the long run.

Finally, a well-thought-out cash management strategy—especially where volatility can be high or increase—may help an active fund manager to create risk-adjusted value. This is over and above a portfolio that only deals with cash strategy as a consequence of cash coming in and potential cash going out from fund holders.

ALLEN ELlSTEIN, MAAA, FSA, is managing director of Life and Health Associates in Brookline, Mass.