By Mark Troutman

This article enumerates many important considerations for a managing general underwriter (MGU) desiring to contract with an insurance carrier to issue and service provider excess of loss (PXS) policies covering catastrophic medical risks assumed by Accountable Care Organizations (ACOs).

The first issue to address is the motivation for seeking to enter into such an arrangement. One common rationale is the ability to package multiple products / complementary product lines (i.e., affinity or cross-selling relationships). There may be several areas to develop cross-sell opportunities with the primary product line envisioned by the MGU of PXS. Examples include:

- HMO reinsurance is particularly important, as many PXS risks can be assigned to captives or other risk-bearing entities, which can then be reinsured on a similar basis as the original PXS risk. This may also occur as “HMO pass-through” reinsurance in situations where the risk first rests with an HMO accepting risk from a government or commercial entity and then capitating ACO providers for that risk. The HMO can provide the quota share (QS) or excess of loss (XL) protection to the ACO provider entity and only pass on the ACO risk net of this reinsurance.

- Employers stop loss (ESL) may be provided in the facility for commercial employer groups related to the risk-bearing ACO provider entity in some way (e.g., hospital or physician group). Say an ACO is offering its managed care discounts and medical management capabilities to commercial employer groups. The carrier and MGU may want to underwrite these risks as well. ESL insurance risks using ACO managed care networks are an excellent niche given their ability to control costs for all claims, including catastrophic claims.

- Cross-selling is possible with other P&C coverages provided by the carrier and/or MGU such as medical malpractice, managed care management liability, other professional liability (D&O / E&O), or property.

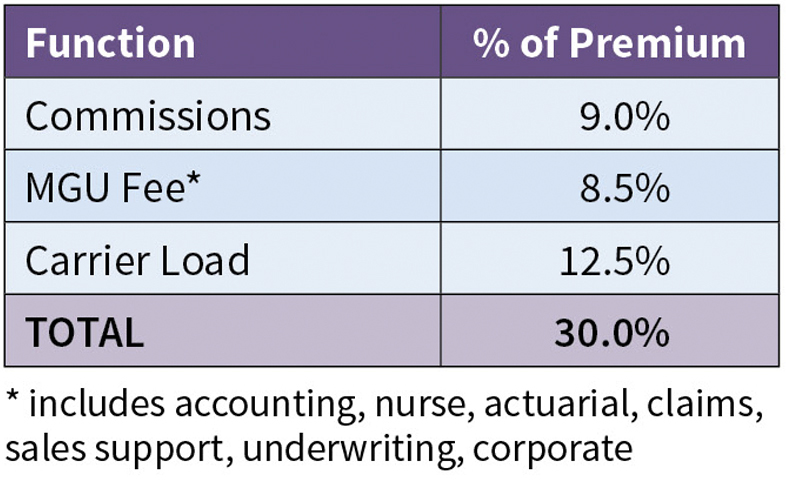

Fee structure

An obvious motivation is to make a profit through underwriting results for the carrier and through service fees and potential profit commissions for the MGU. The following is an illustrative fee structure for a carrier / MGU deal in this marketplace for a broker distribution model:

This structure produces a carrier target loss ratio (claims / premium) of 70% given the expense load of 30% (9.0% commission +8.5% MGU fee +12.5% carrier expense, risk and profit load). ACO insurance is subject to premium tax and the insurance carrier expense load typically accounts for this. HMO reinsurance is not subject to insurance premium taxes. A profit commission may be provided to the MGU for exceptionally good underwriting experience (with deficit carryforward for unfavorable loss experience).

The above assumes the MGU manages most program functions. An MGU fee structure for a deal involving more support by the carrier will be a lower percentage of gross or net premium versus the 8.5% described above. Volume discounts may be offered in several situations. The carrier and MGU typically offer a variable fee and, hence, a variable rate structure based on ACO client premium size. In addition, the MGU and carrier may offer a variable fee structure to each other based on existing block premium volume. A sliding MGU fee example would be 9.5% for block size under $25M, 8.5% for premiums between $25M and $50M and 7.5% for premiums above $50M. The carrier may offer a similar variable expense and profit structure for its economies of scale.

A carrier typically offers the MGU the ability to increase its income via a share in underwriting profits (e.g., 20%-33% ) above some target level designed to meet carrier return on equity requirements before excess profits are shared.

Policy and rate filings

The carrier must have filed PXS (and possibly ESL) policies in all targeted state jurisdictions. Some states allow “file and use” policy forms, some don’t. The carrier will want no marketing conflicts with the MGU. Otherwise, there will be market confusion with clients and brokers.

The carrier and/or MGU must have an actuary on staff to support rate development and policy filings or must engage an actuarial consultant to do so. This may include filing a rate manual in conjunction with an actuarial memorandum in several jurisdictions. If the carrier or MGU have not developed their own rate manual from experience (active and quoted case data), there are manuals available for purchase (ESL, HMO, PXS) from actuarial consultants.

Although aggregate stop-loss risk on an ACO is a relatively new and volatile risk with tremendous exposure (with limited insurance and reinsurance market availability because of this), the filed PXS policy should still plan and provide for both aggregate and specific stop-loss coverage for the ACO. The aggregate here is different than the traditional ESL 125% aggregate in that the ACO risk here could attach at 105% of expected claims on risk demonstration assumed from the government risk-sharing initiatives of the past five to 10 years (slowly but steadily demonstrating support and promotion of ACO growth as part of the Affordable Care Act). With such large exposures in new unknown ACO programs, risk is very large—even exceeding hundreds of millions of dollars, e.g., by attaching at 105% of expected claims. A typical approach may cap exposure at 10% of expected claims for a rate online of 1%-2% of expected claims. The market took off slower than expected, as many ACOs initially only had upside risk (profit potential) but slowly began to take downside risk (loss potential).

Risk appetite

The carrier may require QS and/or XL reinsurance to protect its own gross risk position. An ideal reinsurance situation would be a variable QS that allows the carrier to increase risk exposure with increased block size and comfort. However, the reinsurer will look for some minimum QS position to make the arrangement viable for minimum premium requirements. The key to any successful business arrangement is aligned economic interests. The carrier typically places its own reinsurance and the MGU provides data analysis and advice. If XL is purchased, the XL deductible amount can be calculated from the ground up or as a fixed layer above a client’s accepted risk.

Distribution channel

The vast majority of the ACO market obtains business through brokers. Early on, there were several direct writers (companies writing business through their own sales force rather than through brokers) primarily focused on the existing HMO reinsurance market at the time along with a vibrant broker market in both PXS insurance and HMO reinsurance. The direct writers ultimately moved to a mixed model accepting both broker and direct business. The carrier and MGU will need a coordinated, coherent distribution strategy to access the PXS risks of the ACO targets via appointed brokers.

The carrier is usually the party responsible for establishing broker relationships and quoting rules (first in, preferred, whatever).

The carrier will look for an exclusive relationship with the MGU, and vice versa. Working together on one line and competing on another is a channel conflict, just like a broker market vs. direct writer conflict. The carrier and MGU may not want to be limited unnecessarily by geography, standard industry classification, coverage type (e.g., commercial, Medicare, Medicaid), coverage feature (e.g., unlimited annual maximum, no average daily maximum), or other segmentation in their arrangement unless it makes sense to both parties. Capitalize on the known opportunities together within the “strike zone” of acceptable risks.

The list of brokers to consider as distribution sources would be driven by carrier existing relationships and new business desires, particularly if the carrier has other complementary lines being written such as those listed in the affinity and cross-sell relationships discussion above. They may include large national brokerages, smaller national brokerages, and smaller regional specialty or “boutique” brokerages and “one-off” local brokerages.

The level of coordination and integration across P&C lines (e.g., medical malpractice, E&O / D&O, property, and managed care liability / other professional liability) varies by brokerage. Most have taken great strides over the past five years to present a common and united face to the market regardless of risks being placed for the client. Previously, the letter house brokers handled HMO reinsurance and PXS and other P&C business in separate silos. Brokers are now happy to cross-sell if convenient, but the MGU and carrier should not underestimate the effort to obtain this small stickiness and renewal advantage.

Binding authority

The MGU must be given a set of clear binding authorities for risks to be bound, policies to be issued (if not handled by the carrier), and/or claims to be adjudicated. The key point is that the carrier and MGU must be on the same page—or they are otherwise wasting each other’s time. For example, if they don’t agree completely on most risks to be targeted, the deal will not work. The carrier shouldn’t be using an MGU for its specialty skills unless the carrier appreciates and trusts the MGU to underwrite and service clients within the binding authorities granted in the MGU agreement.

License(s)

This applies to the carrier and the MGU. A new arrangement will likely require a new MGU agreement, as the carrier will likely have to file it with its domiciliary state and the MGU with its domicile per state regulations. The nature of the licenses for the MGU depend on the lines written and the binding authorities or lack thereof (reinsurance intermediary manager [RIM] implies some binding of claims decisions and / or underwriting of risks for HMO or carrier reinsurance just as a MGU agreement does for PXS and / or ESL as filed policies). The carrier and MGU will be in control of their respective destinies through the terms of the MGU agreement. The carrier has an advantage via the control of the policy renewal via its filed policies if it could replace or assume responsibility for the services provided by the MGU in the event of termination (discussed below).

Some reinsurers enter this PXS market by establishing an MGU arrangement and lining up a (less active) “front” insurance carrier with the necessary filed policies. The front company may retain a small portion of the risk or none, if allowed by statute. This may require RIM as well as MGU agreements to be completed. Refer to applicable state insurance department statutes in this regard.

Managed care support services

This is as critical as the underwriting of the risk. These services help the carrier and MGU assess the risk and help them help the client manage the risk. This includes nurses involved in triaging risks at underwriting and at binding (with disclosure). Once a risk is bound, all parties attempt to mitigate the risk with such programs. See any major current carrier / reinsurer website for description of said programs. The carrier / MGU also must determine whether they wish to “schedule” any such managed care services programs in the policy that allows for benefit incentives and disincentives for use or non-use of targeted programs. Primary examples are organ transplant, neonatal, specialty drug, cancer, kidney dialysis, hospital fee negotiation, and provider bill analysis.

Most of these programs are provided by third-party vendors but require considerable skill and effort by the MGU to implement, access, and effectively utilize them to the benefit of all parties. This holds true for carrier, MGU, and client. Even though ACOs are usually integrated delivery systems, there will usually still be need for a variety of catastrophic claim management programs to be provided to carrier / MGU clients to help mitigate catastrophic claim severity and frequency. An on-staff carrier / MGU nurse often coordinates this integration and ongoing support. The nurse works with the ACO clinical staff (nurses and physicians ) in a consultative role. They do not make clinical decisions on care or treatment, and they do not have direct involvement with any insured member. They only advise. Otherwise, they would assume professional liability risk.

It is critical for the MGU staff to assess and fully understand the care management capabilities of the ACO risk-bearing entity, or to suffer the underwriting consequences. Not all ACOs are of like medical management capability and provider cost structure. A rate manual and claim experience will still not capture all of it. Field underwriting is still valuable, which leads to recommendations for managed care programs discussed here.

As mentioned, many of the programs even have some form of coverage incentive for use or disincentive for non-use by the client (e.g., deductible or coinsurance differences). These are accomplished via “scheduling” such features in the coverage. For example, this market initially provided higher coinsurance for use of approved transplant facilities / centers of excellence. In essence, it was a PPO arrangement of 90% coinsurance for approved transplant networks and 50% for all others. Another example is a “drop-down deductible” (i.e., a reduced deductible if the client utilizes preferred vendor facilities).

Incentives are less dramatic now but can still exist. And underwriters still review where transplants are occurring, especially if outside the ACO provider network. There are so many specialized offerings that can improve quality outcomes and reduce costs versus simple discounted fee-for-service arrangements. Transplant network examples include Lifetrac, Optum (UHC), AIG, LifeSource (Cigna), and Interlink.

It is customary to include approved vendor service fees for all such managed care programs as eligible claim costs because they mitigate catastrophic claims.

Utilization of these programs varies by risk population (and concomitant catastrophic claim risk) a la Medicare, Medicaid, dual-eligible, special needs populations (SNPs), or commercial risk. Medicaid is heavily neonatal and factor drugs. Medicare is cancer and cardiovascular. Commercial is all of those plus transplant. All lines are now increased specialty pharmaceutical claims risk.

Termination

This is a key negotiation point between the MGU and the carrier. Each actual PXS client controls the business at termination. They are the ones, one by one, tha decide where to place their future business at each renewal. The typical approach in an MGU deal is that the business is controlled by the MGU that brought the business to the carrier. The carrier (especially if a front carrier) will relinquish any renewal rights to the MGU on said business for one to two years from the date the MGU agreement is terminated. However, if the insurance carrier initially brings the client business and the broker distribution channel relationships to the deal, it will likely retain the renewal rights on the PXS client business upon termination of the MGU contract.

A less common arrangement is to have the MGU agreement be silent on this circumstance. In that case, both MGU and carrier can attempt to renew any inforce business; this sets up a battle for the inforce business when the deal is terminated. The MGU must find new insurance paper for existing and new business post-termination. The carrier must find another MGU or service the business itself. The carrier with its filed policy paper on the street and existing distribution relationships may hold the negotiating power in this regard, but situations certainly vary. Whichever entity is more client-facing will also have an advantage at termination.

Insurance and reinsurance capabilities

As mentioned above on cross-selling, it is critically important for a carrier to be ready, willing, and able to accept such risks on its PXS policy directly as well as reinsuring some risks that may be assigned in some way to a controlled captive or other risk-bearing entity by any name. Similarly, some ACO risks can be covered via HMO pass-through capabilities. Some ACOs and brokers have assigned (transferred) to an ACO-controlled captive said risk an ACO originally accepts. The risk is then able to be reinsured rather than covered by a filed PXS insurance policy of the carrier. Expert legal advice is required.

Insuring a risk and ceding some portion to a client captive (or reinsuring a captive if a risk is placed there somehow) provides an extra level of “stickiness” to the coverage. Similarly, any related unbundled services provided to the captive increase the likelihood of writing a risk and retaining it because it is less a standard commodity. The services in support of captive management include rate development, underwriting by risk layer, premium billing and collection, policy or treaty issue, managed care programs, and claims adjudication.

Carrier profile

This is evidenced by market reputation, rating agency ratings, and knowledge and involvement of senior management in these lines. It is not enough for the MGU to only have good day-to-day working relationships with carrier middle management staff when the day comes for strategic plan approvals, investments, and policy, underwriting, or claim exceptions. A product line viewed as a side dish rather than a main course can be easily exited and leave the MGU to scramble for a new paper and MGU deal (even worse if it happens just before renewal season).

Administration

The MGU and carrier will need to invest in a system or systems designed to manage these product lines. Although premium billing and policy issue may be an easier lift as a modification to an existing MGU system, the claims module is very specialized to handle all types of coverage segments (e.g., Medicare includes AFDC, TANF, ABD, etc.), and managed care claims such as per diems , discounts from billed charges, and diagnosis-related groupings. If neither carrier nor MGU has an existing system with said capabilities, they can pursue lease or subcontract from a small number of vendors in this space.

New drug pipeline

Of critical importance is a carrier / MGU strategy to effectively deal with the emerging catastrophic claim risk represented by gene and cell therapies. Examples include internal and external limits with and without premium surcharges or credits , specialty pharmaceutical deals, or carve-outs with preferred vendors , exclusions, or purchase of reinsurance. Review industry articles on this exploding pipeline of new, very expensive drugs. Gone are the days of inside coverage limits on average daily provider charges called average daily maximums (ADMs).

~ ~ ~ ~ ~

In conclusion, a well-orchestrated arrangement between an experienced MGU in this space and an insurance and reinsurance carrier willing to assume catastrophic ACO claim risk can be a big score for all involved parties.

MARK TROUTMAN is the retired president of Summit Reinsurance Services, an MGU owned by Companion Capital Management, Inc.