By Allen Elstein

Index funds and exchange-traded funds (ETFs) over the past decade have grown to be a large portion of what we can loosely label the mutual fund world. This rapid growth has created several unintended consequences for increased or changed risk in that universe.

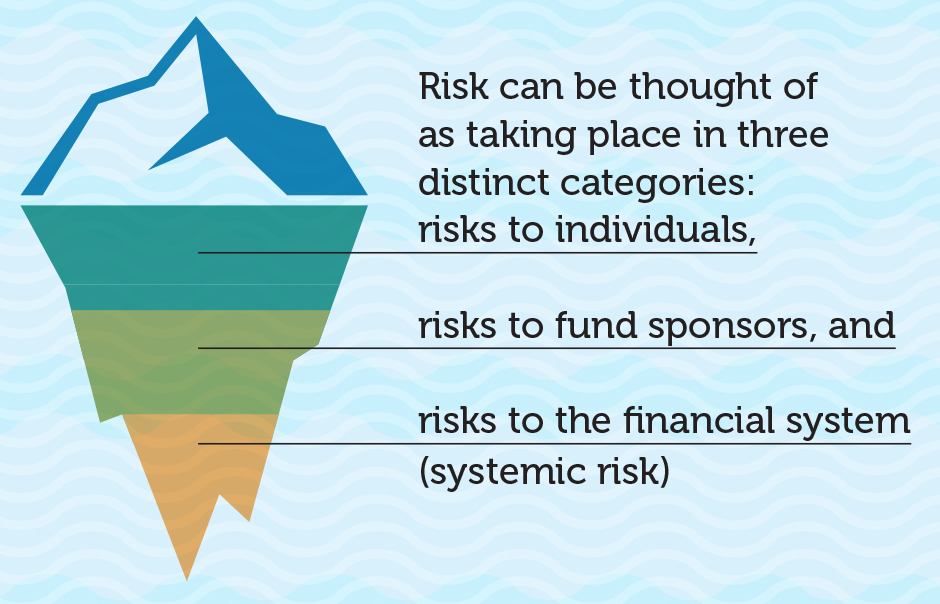

Risk can be thought of as taking place in three distinct categories: risks to individuals, risks to fund sponsors, and risks to the financial system (systemic risk). A particular risk exposure can affect one or more of these categories and can be either well known or not well understood (“hidden”). The recent large exposure in the financial markets has created new, not–well-understood risks for both index funds and ETFs. Due to the way their investment units may be created and deconstructed, as well as the behavior of external short-term traders, ETFs especially have the potential for unique systemic financial stress beyond that associated with index funds.

In a world where they represent a material percentage of both the stock market and end-of-day trading, but where the growth of their popularity may be peaking, index funds may soon experience weak performance hitherto unseen. In addition, to the extent that a market bubble forms in a particular sector, the fund will have both an increasing percent of assets in that sector and increasing exposure to that sector losing material value.

ETF units are often packaged and deconstructed by an opaque set of traders or institutions whose relationship to the ETF distributor is often not well defined or well controlled. In particular, such “market makers” may be semi-independent and without the deep pockets to be true market “backstops” under stress. In normal times, packagers can easily make money buying and selling the underlying stocks to create and deconstruct the ETF units as needed. Under normal volatility, it is easy to make a profit with just a few basis points paid for their “services.” However, under significant volatility—especially on the downside—history has shown that being adverse to large risk, at least some of these market makers may disappear, leading to large short-term drops in asset price.

This article looks at large-capitalization passive funds such as S&P 500 index funds, which I will label “BI” for a model index fund and “BE” for a model ETF. It should be noted that while such funds are passive funds, with a predetermined strategy, they are de facto “active” strategy funds requiring active actions to control levels of risk. Said another way, BI and BE are fully invested funds and need an active person to either move more from a cash position or to sell part of the fund to decrease risk. De facto, the funds’ active strategy is a buy-and-hold strategy.

Index funds differ from actively managed funds, but the differences need to be carefully analyzed. That is, on one end of the spectrum are index funds; on the other are truly actively managed funds. In between are funds that can be thought of as closet index funds. They are often easy to spot from their annual reports, which describe pluses and minuses in return as out of index positions (bets) that either paid off or did not pay off. The in-between funds are often close to index funds with a high correlation to the index. They may have some performance divergence because of intentional or unintentional cash positions.

Mutual fund companies and their portfolio managers have an incentive to keep their performance close to that of the index that for Securities and Exchange Commision (SEC) purposes they have chosen to be measured against. Winning moderately big against an index may somewhat increase sales, but losing for several years relative to an index takes money under management away in often larger quantities. Even if a good stock picker is right 60 percent of the years, the risk of down years gives the portfolio manager and the management company incentive to try to be somewhat close to the index.

If, say, 50 percent of the funds are index funds and 40 percent are closet index funds to a material degree (say an 80 percent correlation to the index), this leaves very few funds that are true actively managed funds, at least outside of hedge funds and private equity.

Index funds are not immune to the economics of supply and demand. In the recent period during which people have bought into the index fund advantages, this means that the basket of stocks of the index will rise in price with the increased popular demand—perhaps more so than other stocks. Thus, one can expect that in a time of increased popularity, we should have seen a portion of superior performance, even without the expense advantage—and indeed we have.

But now we have to ask what will happen if that popularity either levels off or goes down relative to some external event.

Actively managed mutual funds suffer from a particular disadvantage over their corresponding index in a rising market, such that a material portion of the rise may be in a few closely correlated stocks such as Facebook, Amazon, and Apple. To the extent that these stocks are in vogue, they can rise quickly and have relative to their potential a very full price. For the active managed fund, in a vacuum they might believe that a 2 to 3 percent position in Apple is optimal from a risk perspective. But to beat an index that has 5 percent of its holdings in Apple, the active manager would have to increase his or her stake accordingly. This pressure in and of itself can raise the price of Apple even more. For the entire category of nifty technology stocks, this might mean needing to be weighted 15 percent in just four stocks merely to beat the index.

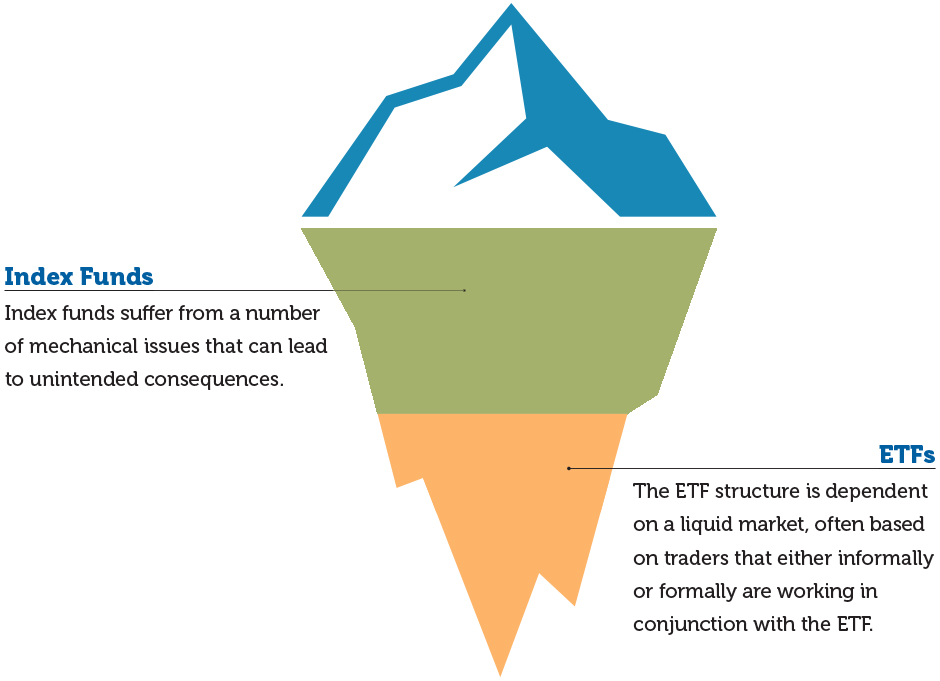

Index funds suffer from a number of mechanical issues that can lead to unintended consequences. For example, assume that the market is made up of 10 sectors. In an ideal world of risk spreading, one might have 10 percent in each sector. But in a world of high technology boom, one can see the technology sector go from, say, 10 percent to 20 percent. Any downturn in technology could then have a larger-than-ideal effect on the index. Similarly, to the extent that the index weighs the largest 10 percent of the stocks by market capitalization, any downturn of the largest stocks (think reversal of momentum) could have a larger-than-ideal effect.

In a world where the technology stocks known as FANG—Facebook, Amazon, Netflix, and Google—can be a large portion by themselves of an index, one can see both extra upside and extra downside volatility relative to a more nuanced investment strategy. Finally, even in normal times, the weight of the various sectors in most indexes is not equal, which might mean that the “diversification” of index funds could be suboptimal, even if not market capitalization-weighted.

Being part of an index also affects how the stock price of a stock changes. Consider an index where there are only two stocks, x and y. Each at the beginning of the day is 50 percent of the index. If x goes up wildly—and even if y would otherwise go down slightly—because y is part of the index, y might also go up. Even so mechanically, some y has to be sold because now x is more part of the index. Said differently, being part of an index (that owns a significant portion of the stock of that company) distorts what the true price of the stock would be in the absence of it being in the index. In the long run, this might have to be reversed.

To the extent that our indexes BI and BE are governed by mechanical rules that in effect cause end-of-day rebalancing, in that very end of the day when a lot of the trading on the stock exchanges takes place, active traders have an opportunity to front-run the indexes. To date that threat has not been as disruptive as one might fear, but it appears that this is an activity that could cause issues down the line.

Thus, index funds, at least as their mechanics are currently defined, are passive investments but default to an always fully invested strategy unless there is someone managing to and from a cash position.

ETFs present added issues. There are many possible ways of structuring an ETF. For the sake of simplicity, I will define one such strategy. It should be noted that the old-fashioned market makers of the major exchanges no longer exist, so an ETF company is either dependent on independent traders or ones that it contracts with. We will assume that there is a contract with some such traders, and we will label these traders “primary investors.” This leaves the BE fund customers like you and me, who will be labeled the secondary investors. Primary investors have to be involved only to the extent that there is a net purchase or sale of BE shares in a given period of time. Assuming there is a sale, the BE customer is given cash and the primary investors are given the underlying stocks, which it can sell on the open market for a few basis points of profit.

The primary investors are happy to serve as this intermediary in this scenario if there is no unusual volatility. They normally make 2 basis points, for example, but if there are some curves, or some sophisticated investors trying to front-run them, they might make 1 basis point, or maybe none at all. But what happens when there is a market scare or uncertainty?

Just like the derivative traders during 2008 and 2009, there is not a lot of capital and at least some of these primary investors or related traders disappear. If that happens, the smooth trading of the ETFs disappear. At least at the end of the day, index fund investors have the advantage of having a market value that is the sum of the market value of what stocks the index fund owns. This may be an advantage for an index fund that a buy-and-hold investor who could choose either an ETF or an index fund might consider in determining a vehicle of choice.

So, it appears there are risks and anomalies in index funds that are not normally talked about. In addition, as the popularity slows down, the advantage over a true active management style could deteriorate, especially if lower-cost active strategies appear. Worse, the ETF structure is dependent on a liquid market, often based on traders that either informally or formally are working in conjunction with the ETF. They do not necessarily have the capital to sustain smoothness or an orderly market, and we could see more cases where the ETF values differ greatly from what would be suggested by the underlying stocks. At least with an index fund, at the end of the day, the value is close to the underlying stocks would suggest.

With respect to ETFs and index funds being low-cost options, that may not be true if total costs, and not just fund expenses, are considered. ETFs and index funds in recent years have been packaged as the primary vehicles that some financial advisers charge a 1 percent asset management fee for. With an average expense fund expense charge of 0.3 percent, that amounts to a total cost of 1.3 percent. A client with a $200,000 account and a 30 percent annual investment rollover rate might have paid considerably less than that in the old days for commissions and a few hours of advice a year. The annual asset fee is likely much more attractive to advisers than commissions, especially because computer-generated portfolios—customized for age and other factors—are marginally cheap to create and modify.

Individual stock price volatility is affected by the large popularity of passive investment funds. Under extreme market stress, market volatility patterns may dominate. However, under moderate stress, several theoretical predictors of individual stock price vulnerability due to passive investments exist. If the percent of stock A shares held in passive funds is higher than stock B, it may exhibit more market price volatility. However, if both stocks have 40% of their shares held by passive funds, then “market liquidity” of the stocks may result in different volatility vulnerability. In practice, however, individual stock price volatility, when either the stock or the market is under stress, is very hard to predict. That is, the relationship among the portion of the stock in indexes, the portion held by traders, and the portion held by long-term investors—even if known—does not lead to clean models on whether or if that stock is more or less vulnerable to downside volatility than if the percentage of ownership among the various categories of owners were different.

Index funds and ETFs are, of course, very much dependent on the index they’re based upon. To the extent that the underlying index is well known, some investors may believe that they are getting good exposure to the category of small–cap stocks if they simply buy a small-cap index fund or ETF, for example, and that the index has not materially changed over time. This may not always be the case. And this is true of other indexes as well.

T. Rowe Price, the historically active management mutual fund company, in its T. Rowe Price Report to clients (Issue Number 137, Fall 2017) in a section titled “Declining Number of Traded U.S. Equities” that discusses its impact on small-caps concludes that this shift has produced a structural deterioration in the quality of firms in, for example, the Russell 2000 Index. In particular, T. Rowe Price states that the number of public companies in the Wilshire 5000 (an attempt at a total market index) has declined from about 7,500 in 1998 to about 3,464 as of June 2017. There are several causes for the shrinking universe of publicly traded stocks, including two fundamental ones:

- The decline in the amount of public offerings in the small-cap universe due to companies staying private longer, including the increased use of venture capital in a world with low borrowing costs; and

- The loss of stocks due to mergers, acquisitions, companies being taken private.

T. Rowe Price, in specifically discussing the Russell 2000, states, “The shrinking equity market has had a disproportionate impact on the Russell 2000. While the index is rebalanced annually in June to include 2,000 names, the companies added to the index in recent years have tended to be smaller, more illiquid, and of lower quality than the firms they replaced. Further, the company notes that

“[a]bout one-third of the companies in the index have not earned in the money in the past 12 months, a level normally only seen in recessions. … While active portfolio managers may [avoid] the lower-quality members of the index, passive products have been natural buyers of their shares” [because the stocks are in the Russell 2000]. This has helped drive up the shares of mediocre companies … posing significant risk for passive investors.”

In particular, “in the next sustained market downturn, passive products seeking to sell to fund outflows may have trouble finding buyers for the lower-quality, less liquid stocks in the rush to the exits,” T. Rowe Price warns.

It should be noted that index funds are not the first value-added insight in mutual funds investment. Often a value-added idea comes along, works because it creates value, and then work for a while longer because people pile on, creating a further price increase. These insights work—until they don’t. Examples are the 1960s with the growth stock revolution. The insight was that growth stocks could support a higher price-to-earnings ratio and outperform in the medium term. It worked, then people piled on (things appearing to work)—until the price-to-earningss ratios went too high, and then growth stocks underperformed.

What are some of the fundamental questions for ETFs: Just who are the people who are creating and dismantling investment units for retail investors? Just how are these people related to the fund? How deep are these market makers’ “available” assets? And how willing and able are these people to stabilize price volatility under severe selling stress in the market?

Similarly, what are some of the fundamental questions for indexes and the funds named for them: Do some stock or sector components have an outsized weight? How has the index and average characteristics of its components changed over time? Has the price of the index or individual stock components materially changed merely because the index has allowed people to indirectly invest in previously harder-to-invest components of the stock market? Are some stocks in the index significantly overvalued merely for being in the index? How would these overvalued stocks fare in a severe downturn, and what would be the effect on the overall index?

In summary, we have historically looked at index funds and ETFs in a way that emphasizes their good qualities. Prudence suggests that we should also ask what can go wrong. Are we looking at these funds as the market behemoths with hidden risks that they are, or as the quirky bit players they were when they launched a few decades ago?

ALLEN ELSTEIN, MAAA, FSA, is managing director of Life and Health Associates in Brookline, Mass.